“Office markets continued to suffer from the uncertain political and economic environment in some European countries, and investors remained cautious on the asset category, which has been affected by structural changes in the way people work over the last five years. Overall, 2024 ended with a stabilisation in take-up and a slight increase in the volumes invested in offices. There could be a more pronounced recovery in 2025 if the economic and financial situation lastingly improves.” says Argie Taylor, Head of BNP Paribas Real Estate’s International Investment Group.

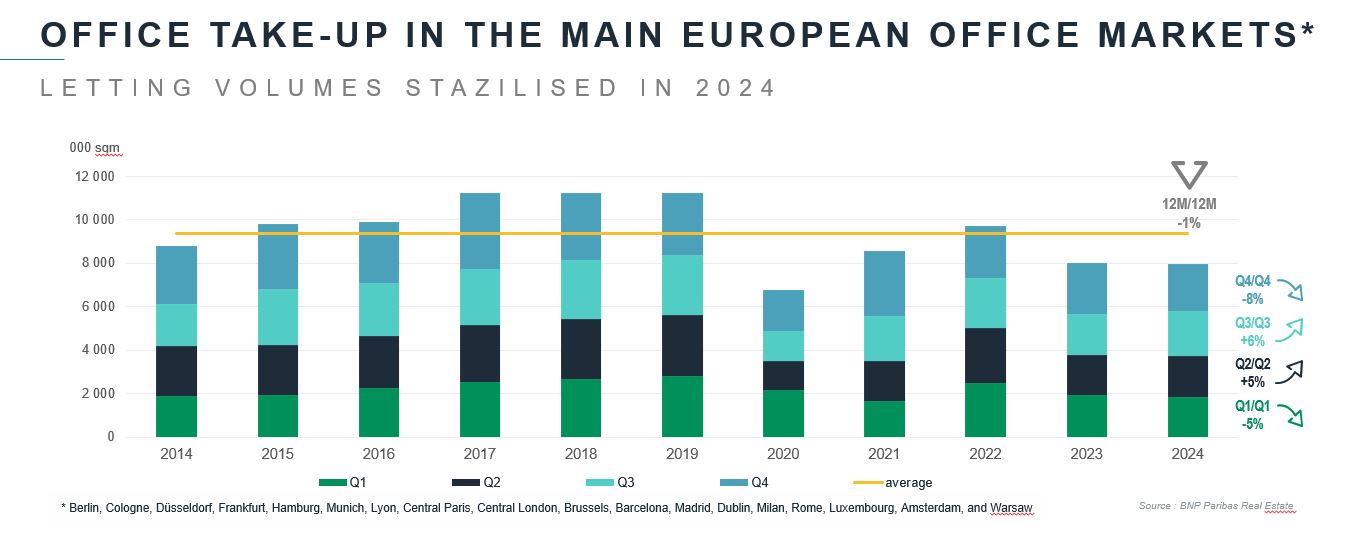

Stable take-up in 2024

After an encouraging recovery in the second and third quarters of 2024, the rental market in Europe slowed in Q4, falling by -8%, with some major markets such as Paris and the German cities still hampered by political and economic uncertainty.

All told, take-up in 2024 was almost unchanged compared with the previous year, at 7.96 million sqm in the 18 leading European markets*.

Some markets rallied strongly, such as Dublin (+58% after a gloomy 2023), Amsterdam (+17%), Berlin (+7%) and Brussels (+6%). Lyon (+2%), Cologne (+1%) and Barcelona (+1%) managed to hold their own, while Paris and its Inner Rim together with London saw respective declines of -7% and -6%.

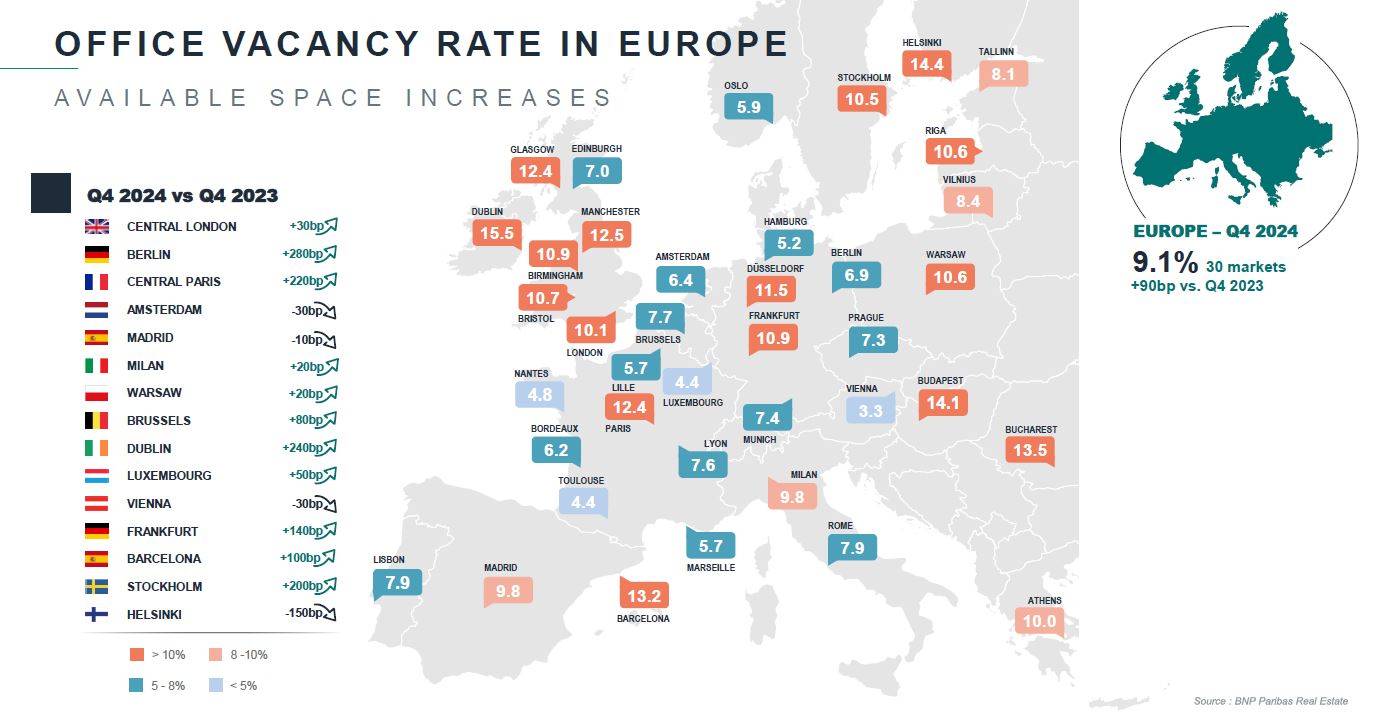

Growing supply

The overall vacancy rate in Europe at the end of 2024 was 9.1%, up 90 basis points year-on-year. “The biggest increases in Berlin (+280 bp year-on-year) and Dublin (+240 bp) were due to large-scale completions of new buildings in recent quarters,” notes Argie Taylor.

There is a divergence between the CBDs (central business districts) of the 13 main European markets, which have an average vacancy rate of 5.4%, and the outlying districts in these cities, where the average vacancy rate is 10.5%. This trend has intensified each quarter (from 350 bp in 2020, the difference stood at almost 500 bp at the end of 2024), reflecting growing polarisation in several cities. The best-quality assets in the most central and accessible districts continue to find takers, unlike second-hand buildings or those in suburban locations, which are suffering from waning occupier interest.

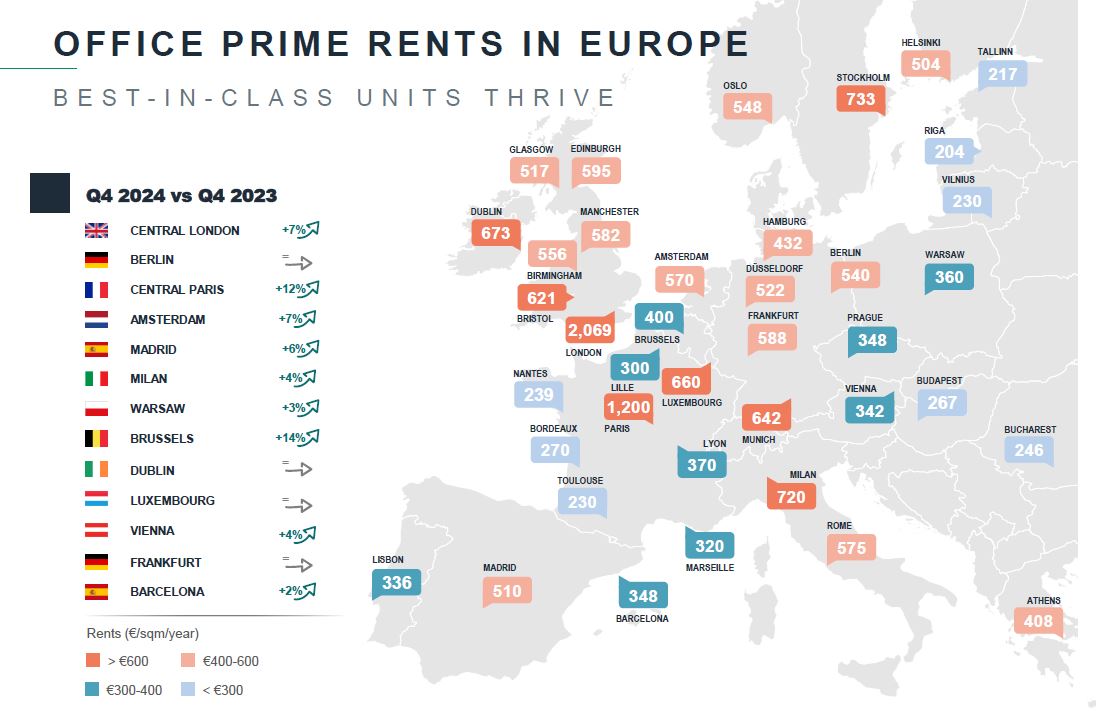

Prime rents still rising

The preference for a central location and high quality continues to underpin the upward trend in prime rents in most European cities.

The biggest year-on-year increases were in Brussels (+14%), Paris (+12%), London and Amsterdam (+7%), and Madrid (+6%). Overall, rents rose by 5.4% in 2024 for prime offices in the main markets, vs an average of +3.3% for all assets.

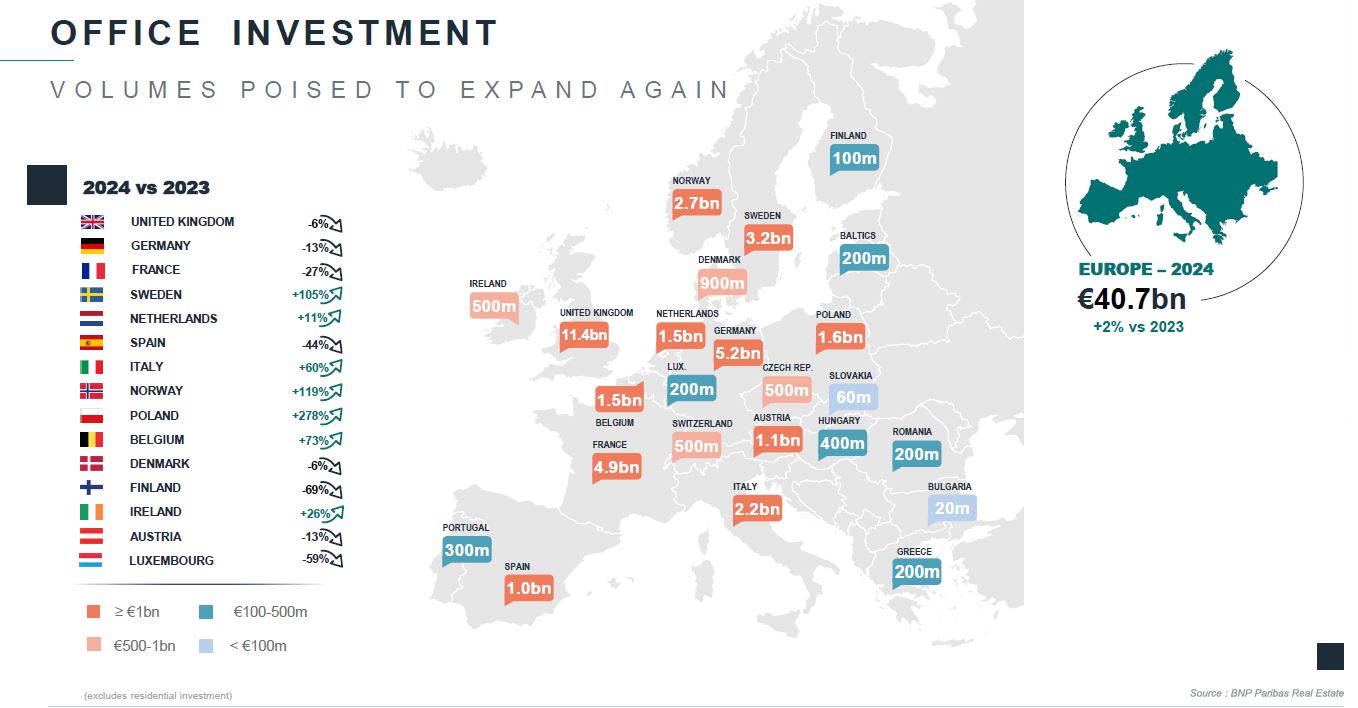

Investment rising again

After bottoming out in 2023, investment in commercial real estate was up 21% at the end of 2024 compared with 2023, standing at € 157.4bn. This recovery applied to all asset categories. The adjustment of capital values continues, combined with an improved outlook for yields and lower borrowing costs, encouraging the return of investment capital.

Investment in offices in Europe in 2024 came in at € 40.7bn, up +2% on last year and the first year-on-year growth since 2022. “The share of offices in overall commercial real estate investment is now 26%, much lower than it was in 2019 (49%), reflecting investors’ ongoing cautious approach to the asset category”, indicates Argie Taylor.

The slide in the three main European markets (UK, Germany and France) continues, despite easing significantly in H2 2024. Conversely, investment has increased greatly in other markets, particularly Poland (+278%), Norway (+119%) and Sweden (+105%). More moderate, but nevertheless impressive growth was also seen in Belgium, Italy and Ireland, up +73%, +60% and +23% respectively.

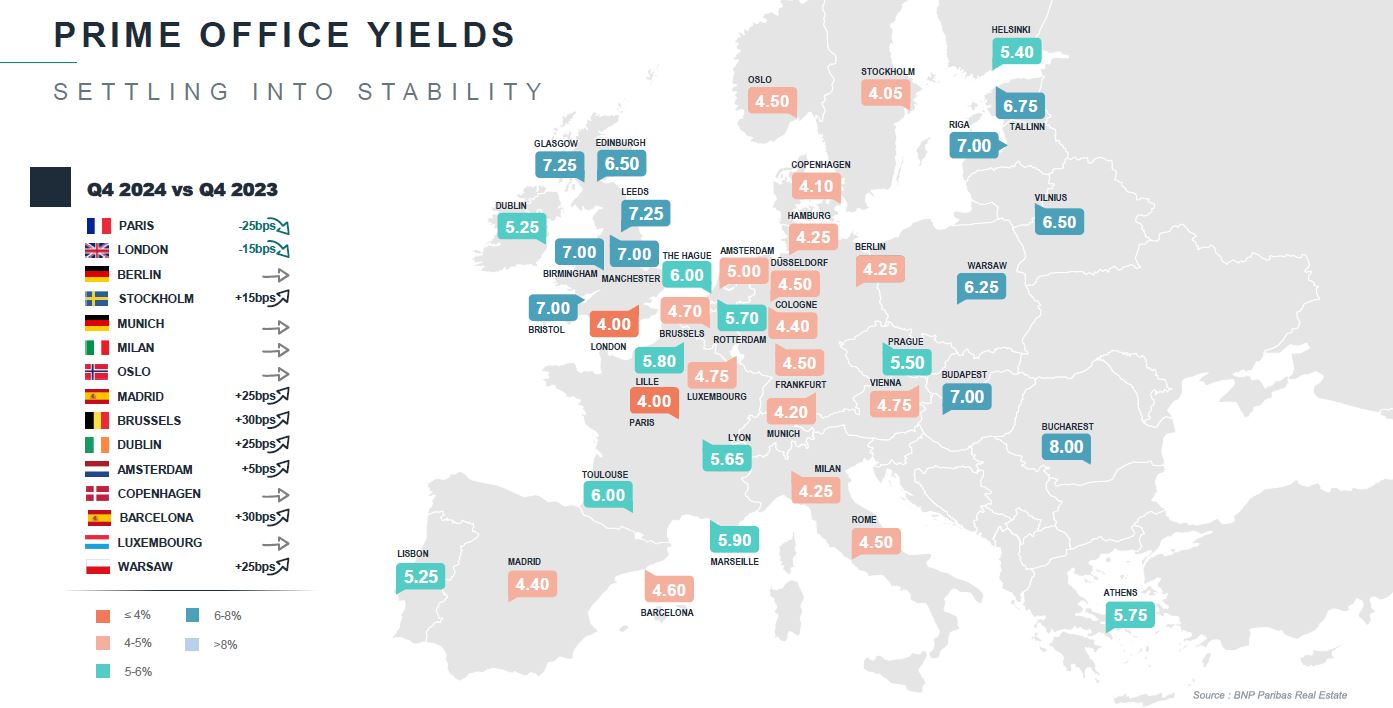

Prime office yields have levelled off

The improved macroeconomic backdrop and the fall in borrowing costs meant that prime yields generally stabilised through 2024. Office yields have plateaued since the end of 2023.

Paris and London had prime yields of 4.00% after the first signs of contraction in Q3, displacing Stockholm (4.05%), which had boasted the lowest yield for the previous year. These three cities are closely followed by Copenhagen (4.10%) and Munich (4.20%).

“The gradual upturn in investment and the expected interest rate cuts should keep yields stable in 2025 and even allow a gradual contraction to begin in some markets,” concluded Argie Taylor.

- Amira TAHIROVIC