LOGISTICS WAREHOUSING MARKET IN EUROPE SETS NEW RECORDS

The occupier market set a new transaction record in 2021 increasing by 29% in the six leading countries, with a number of regions posting new highs in take-up. Yet construction rates for warehouses are lagging demand and speculative developments remain limited. The shortage of materials is further exacerbating the situation by creating delays in new developments, while access to land is another limiting factor. A tight demand and supply balance means rental pressures are building.

Take up in six countries in 2021: +29% (vs 2020)

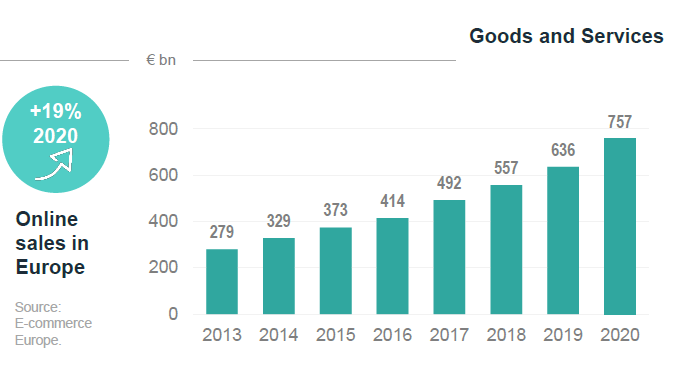

Yet another transaction record was set in Europe in 2021 with growth in every country, boosted by online sales and an overall economic upturn.

The marked changes in consumer behaviour triggered by the Covid-19 crisis favoured on-line shopping and helped e-commerce further penetrate less common markets, further boosting demand for logistics space.

Supply drying up over the past three years while demand has remained keen and caused major imbalances in some markets. This was particularly evident in prime areas, where demand shifted towards other regional locations.

Completion timeframes and availability of land will dictate the market balance in areas where the vacancy rate is well below the European average of 5% recorded in 2021.

New developments are still insufficient to meet demand, yet little speculative developments have been launched.

Country profiles in 2021

In Germany, the logistics market ran at full speed to reach a new record volume of transactions in 2021, boosted by e-commerce. The logistics sector came through the crisis better than almost all other sectors of the economy.

The UK broke a new record in 2021 at 6 million sqm. Market growth was underpinned by a strong economic upturn (+7.1% in 2021). With the development pipeline for new stock contracting slightly and occupier sentiment remaining strong, long-term returns look stable as rental growth continues

In Poland, take-up achieved another record year. The pandemic fuelled the already solid growth of e-commerce and the robust economic growth (+5.2% in 2021) further supported the market.

In France, after a slow start to the year, the market gained momentum supported by strong activity in Paris and Lille and robust GDP growth (+6.7% in 2021), one of the highest in Europe. Overall, supply remains scarce in most submarkets.

In the Netherlands, take-up set a new record in 2021. Due to low availability in the main logistics hotspots, take-up continued to shift towards less established locations. Rents stabilised but strong demand and low availability are still causing some upwards pressure.

In Spain, transaction volumes set a new record of above 2 million sqm in 2021. Activity was stimulated by e-commerce and food retailers as well as strong economic growth (+4.3% in 2021). Vacancy rates are still very low, helping to drive upward pressure in rents, particularly in Barcelona.

Prime rents rose by 3.4% in 2021 across a panel of 49 markets covering 22 countries.

Industrial and logistics investment set another record with € 65bn invested in 2021, +51% compared to 2020, but ongoing demand will only be satisfied to a limited extent. “The industrial and logistics market is still gaining market share against other assets. The category rose from 18% to 24% of total investment in commercial real estate in one year. The shortage of products available in prime locations resulted in yield compression. Prime yields dropped across Europe by 60 bps on average over 2021. Further yield compression is anticipated as competitive pricing remains tough”, comments Craig Maguire, Head of European Logistics at BNP Paribas Real Estate.

Strong market drivers

Strong market drivers

The acceleration of vaccination campaigns across Europe combined with the economic upturn across Europe in 2021 stimulated demand for warehouses. Covid-19 accelerated the shift to e-commerce and put the spotlight on supply chains. Shoppers turned to internet sales and traditional retailers developed internet solutions for their customers. The transformation of the retail sector by e-commerce development is far from complete. It will continue to affect demand for logistics space for at least the next five years.

Logistics organisation will be transformed in the longer term

Rather than holding more inventory to counter supply chain disruptions, companies may establish dedicated logistics networks that minimize distribution costs and move goods faster. Thus, supply chain optimisation remains a strong driver for future take-up of logistics space, particularly at local and regional levels.

The design and operation of logistics platforms are key to how supply chains perform. Development by end users will contribute to supply chain transformation.

In recent years, a large part of demand for space in the sector has been driven by warehousing to store and distribute finished goods manufactured much further away. The COVID crisis prompted companies to on-shore part of their manufacturing processes. As such, we see increased long-term demand for industrial space as a base for manufacturing, altering the nature of some of the units required.

The virus outbreak furthered the penetration of e-commerce

Demand for logistics space is fuelled by on-line business. E-commerce covers a broad range of goods and the corona crisis has had a positive (albeit occasionally mixed) impact. It has accelerated demand in some areas and stalled it in others, depending on the item purchased and where it is moving from.

The medium to long-term changes in consumer behaviour will normalise on-line shopping. They will help to increase the penetration of e-commerce in markets where this has been limited so far, further boosting demand for logistics space.

The need to move the logistics chain closer to the end consumer is creating even greater demand for “last mile” logistics, not only for delivery but for collection too. It may be that more warehousing specifically dedicated to reverse logistics is required.

- Amira TAHIROVIC