Logistics letting markets have generally held up well despite weak economic growth which is expected to remain positive in 2024. Indeed, GDP growth started to pick up in the Euro area at the beginning of the year from +0.5% in 2023 to +0.8 % forecast in 2024.

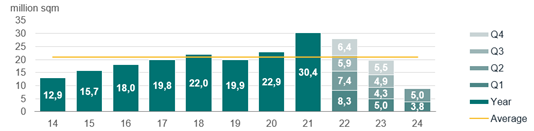

Occupier concerns about cost control in a still weak economy are slowing expansion. In H1 2024, the market decreased by 5% versus H1 2023. Demand has been lagging and most countries recorded a slow start to the year. Yet, market fundamentals remain healthy despite rising supply in some countries and there are signs of inventories increasing in the second half of 2025.

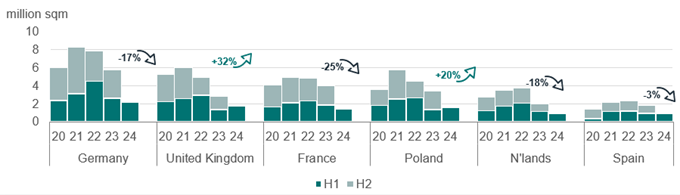

- In Germany, after a cautious start to the year, the market picked up in Q2 2024, particularly outside the main logistics hubs. The weak economy continues to have a slowing effect on demand. The lack of available space remains a limiting factor in some markets, which in turn has been supporting rental growth.

- In the UK, the market bottomed out in Q2 2023 and has been picking up since then. Take-up increased in H1 2024 supported by strong demand from the Food & Beverages industry and continued logistics demand in the Midlands in particular. Supply is stabilizing after ticking up for two years. There is still a lack of speculatively developed new units.

- In France, market slowdown in H1 2024 has been unsurprising as the economy remained slow. Demand dropped significantly in Greater Paris, Marseille and Lyon with well below average levels of transactions. Lille and Orléans on the other hand concentrated nearly half of France’s transaction volume during the half of the year. Overall, land is becoming scarce, and the lack of supply has become recurrent in some markets. The vacancy rate in France reached 4.1% at mid-year.

- The Netherlands, like most European countries, is recording a slow start in H1 2024. High land prices and development costs are inhibiting new developments. Low availability is still putting pressure upwards on rents.

- In Spain, after a slow start to the year, the Spanish market bounced back in Q2 2024 maintaining a good volume of transactions, particularly in Madrid and Valencia. Vacancy rates eased just 5.4% in Barcelona and at 8% in Madrid, whilst supply remained tight in Valencia. Prime rents stabilized in Barcelona and Valencia but increased in Madrid during Q2 2024.

- In Poland, the occupier market picked up in Q2 2024 after a slow start in Q1. The vacancy rate remained at around 8% and prime rents stabilized. A noticeable trend is the sharp decrease in the share of new construction projects launched on a speculative basis. However, the volume of take-up at 1,6 million sqm represented a 20% increase vs H1 2023 and places Poland at the 3rd position in Europe.

Vacancy rates have risen over the past 12 months to a European average of 5.9% as a result of moderate demand. However, the lack of new developments, as land is increasingly regulated in Europe, may continue to underpin rental growth in prime sectors.

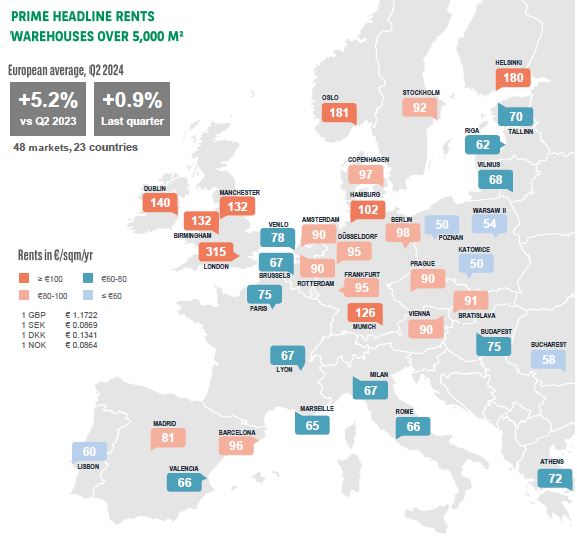

Prime rents rose by 5.2% (y/y) in Q2 2024 across a panel of 49 markets covering 22 countries. Rents are still rising in some cities but overall, the market slowdown in Q2 2024 resulted in limited rental growth of only 0.9% for the quarter. Logistics occupiers are still willing to accept higher rents on existing buildings to switch to green sources of energy. In the future, this could not only mean further potential for increasing rents, but also spur the owners of existing buildings to carry out renovations for greater energy efficiency.

Prime rents rose by 5.2% (y/y) in Q2 2024 across a panel of 49 markets covering 22 countries. Rents are still rising in some cities but overall, the market slowdown in Q2 2024 resulted in limited rental growth of only 0.9% for the quarter. Logistics occupiers are still willing to accept higher rents on existing buildings to switch to green sources of energy. In the future, this could not only mean further potential for increasing rents, but also spur the owners of existing buildings to carry out renovations for greater energy efficiency.

Despite the slowdown in the market, we still see pockets of rental growth and global capital strongly interested in European Logistics markets, says Craig Maguire, Head of European Logistics at BNP Paribas Real Estate.

Logistics Capital markets: some signs of improvement

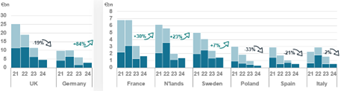

Industrial & logistics investment increased by 6% in Europe during H1 2024 to reach €16bn at mid-year. It may have hit its lowest point in 2023 and is expected to pick up gradually throughout the rest of 2024. This reflects an improvement in financial conditions. The expected drop in central bank key rates in H2 2024 should boost jumbo deals and encourage the return of pan-European portfolios. Deals may take longer to conclude but demand is starting to knock on the door of some markets: France, Sweden, Germany and the Netherlands. This trend is expected to spread to more countries throughout 2024. Nevertheless, we expect investment for the full year 2024 to be significantly lower than in previous years. A material recovery in investment is not expected until 2025.

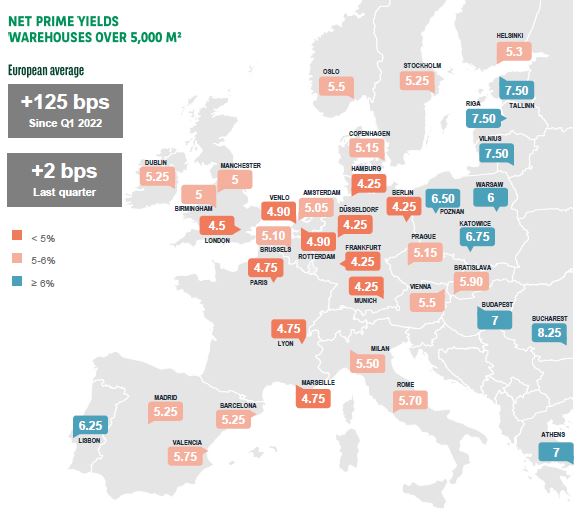

- In the United Kingdom, the industrial and logistics investment market started 2024 at a slow pace, challenged by increased scarcity of new best-in-class stock and economic uncertainties. The Net prime yields stabilized at 4.5% and is now holding firm, which should help unlock investment activity and initiate the beginning of a recovery.

- In Germany, the market increased significantly in H1 2024. The pricing adjustment process with the changed interest rate environment is complete in Germany and demand is strengthening. Prime yields remained stable at 4.25% in the main logistics locations.

- In France, Industrial and logistics resisted market decline well compared to retail and offices. The volume of investment increased significantly in H1 2024. Logistics prime yields remained stable at 4.75% in Q2 2024.

- In the Netherlands the market increased steadily in H1 2024, the capital market seemed to ease with more availabilities for core products. The logistics prime yield remained stable at 4.9% in Q2 2024.

- In Spain, the volume of investment in industrial and logistics remains robust just below its 10-year average. Like the main European markets, prime yields stabilized at 5.25% in H1.

- In Poland, Investment volumes improved over Q2 reflecting better sentiment in the market. Q2 will probably be seen by end 2024 as a market turning point. The prime yield stabilized at 6% in Q1 2024.

Logistics prime yield rates have stabilized in Europe. Interest rate pressure and the associated rising yields on long-term government bonds gradually eased again somewhat. The resulting expansion of prime logistics yields over the past two years also seems to be coming to an end. Prime yields should therefore continue to stabilise throughout Europe until the end of 2024. Prime yields could fall slightly again from 2025. In Europe we expect average compression of around -10bps for each of the next three years.

Logistics prime yield rates have stabilized in Europe. Interest rate pressure and the associated rising yields on long-term government bonds gradually eased again somewhat. The resulting expansion of prime logistics yields over the past two years also seems to be coming to an end. Prime yields should therefore continue to stabilise throughout Europe until the end of 2024. Prime yields could fall slightly again from 2025. In Europe we expect average compression of around -10bps for each of the next three years.

“However, the fundamentals for European Logistics markets remain relatively good. As such, the prospects for Logistics investment look bright, at least from 2025 onwards as we enter a new cycle”, concludes Craig Maguire.

- Amira TAHIROVIC