Every year, BNP Paribas Real Estate publishes the European Office Market Report, presenting the key office and investment market trends in Europe with a focus on 42* cities.

* Amsterdam, Athens, Barcelona, Belgrade, Berlin, Birmingham, Bratislava, Brussels, Bucharest, Budapest, Copenhagen, Dublin, Edinburgh, Frankfurt, Geneva, Glasgow, Hamburg, Helsinki, Lille, Lisbon, Central London, Luxembourg, Lyon, Madrid, Manchester, Marseille, Milan, Moscow, Munich, Nicosia, Oslo, Central Paris, Prague, Riga, Rome, St Petersburg, Stockholm, Tallinn, Toulouse, Vienna, Vilnius, Warsaw.

No slowdown in European office market activity in 2018

The letting market in 2018 almost as dynamic as in 2017

The office letting market in Europe is flourishing, according to the 2019 edition of the European Office Market report issued by BNP Paribas Real Estate. Indeed, office take-up in the 42 main European cities reached nearly 13 million sq m, a similar level as in 2017, which had been by far the most active year in the decade.

At city level, Central London reached 1.4 million sqm (+19% over 1 year) and increased for the 3rd year in a row. Due to a lack of supply, the four main German markets (Berlin, Frankfurt, Hamburg, Munich) combined dropped 8% but still represented 3.04 million m², well above the long term average. Volumes in Central Paris diminished by 9%, notably due to the lack of very large deals. Very high results were achieved in Vienna (+54%), Luxembourg, Lisbon (+21%), Milan and Warsaw (+10%).

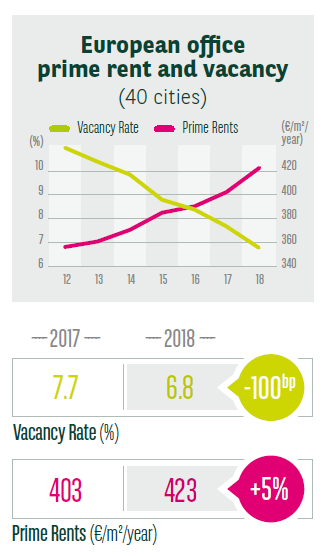

Historically low vacancy in Europe and increasing prime rents

Vacancy shrunk again across Europe in 2018 and may have reached its floor in several markets. The lowest vacancy rates were seen in Germany, especially Berlin (1.7%, representing only 327,000 m² of immediately available office supply) and Munich (2.3%). With only 3.7% of empty office, Luxembourg is close to the level of German markets. The most impressive drop in vacancy was seen in Amsterdam (-310 bps) and Warsaw (-340 bps). In the meantime, the share of empty premises fell in all the other main markets, such as Central Paris (-100 bps), Central London (-120 bps), Milan (-110 bps) and Dublin (-170 bps).

Driven by the high demand for offices and the decrease in vacancy, prime rental values increased in all main European markets, excepted in Central London (-2% vs. the end of 2018) where prime rents reached £1,211/m²/year. Madrid (+13%, €432/m²/year) saw the most significant growth in rental values. Other big increases were in Hamburg, Berlin (+9%), Milan and Frankfurt (+7%).

Another stunning year for investment

Paris back to being the leading European city market, outstanding results in Germany

The investment market followed the same trend as invested volumes remained at a high level, with €264.5bn invested in Europe.

“Activity actually strengthened in the sixteen largest city markets as with a 10% increase they broke the €100bn bar; an absolute historic record. Offices represented 45% of invested volumes in Europe and were characterized by a large share of mega deals. Paris benefited from an impressive growth of invested volumes (+26% y.o.y) and was the most active European market in 2018, followed by London. German markets performed extraordinarily well again as 2018 has been an all-time high for the country, passing 2007 result” analyzes Larry Young, Head of International Investment Group at BNP Paribas Real Estate.

Frankfurt (+38%) was number one ahead of Berlin (-6%) which was hampered by the lack of product to buy. 2018 has been a good year for Dublin market (+81%) that concentrates almost 90% of the Irish market. The Luxembourg market reached its highest level since 2007 with offices representing 94% of the turnover.

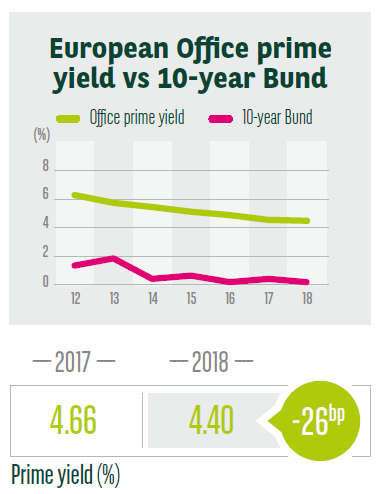

Historic lows in office prime yields

Office yields continued their downward trend throughout Europe, reaching historic lows at the end of 2018. Prime yields stood at 4.40% in Q4 2018 on average among the 40 markets analyzed in this report, 26 bps down on Q4 2017. Among the largest markets, Berlin still has the lowest prime office yield (2.70%) followed by Munich (2.80%), Frankfurt (2.95%) and Paris (3.00%).

“Since 2015, yield compression created value almost passively, affected by plummeting long term interest rates. From now on, more work on the asset, its leases and its revenues will be required to create value. Promisingly, most letting markets are healthy, vacancy rates are unlikely to change much despite forthcoming supply and there is still decent rental growth potential for flagship locations as well as those in development”, comments Richard Malle, Global Head of Research at BNP Paribas Real Estate.

- Amira TAHIROVIC