RETAIL MARKET IN EUROPE: A MIXED PICTURE FOR INVESTMENT, OCCUPIERS FARING BETTER THANKS TO LUXURY AND TOURISM

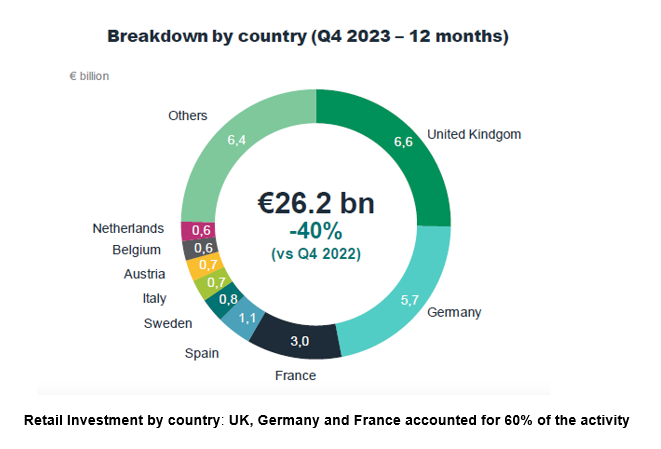

Investment: retail is the second least affected sector after hotels with € 26.2bn invested in 2023

Investment in European retail fell 40% in 2023 vs 2022, to € 26.2bn. Yet investor interest in retail assets is slowly gaining more traction in terms of investment market share (20% in Q4 23 vs 16% in Q4 22). “This level has not been seen for five years (20% in 2018). As a result, retail was the second least affected sector after hotels”, says Patrick Delcol, Head of European Retail at BNP Paribas Real Estate.

Investment in retail warehouses in the largest European countries* came to € 8.5bn over 2023. This segment, although down 28% vs 2022, showed the greatest resilience among the retail subsegments. It accounted for 50% of overall investment in retail assets and is proving increasingly attractive to investors.

The high street segment has seen the biggest year-on-year decline (-50%) with investment of € 4.9bn. However, this fall should be seen in the light of the exceptional 2022 figure (€ 9.7bn). We note that this number does not include the € 2.9bn of owner-occupier deals transacted by luxury brands on the most prestigious Paris avenues.

Lastly, the shopping centre segment recorded a fall of 55% vs. 2022, with investment of € 4bn.

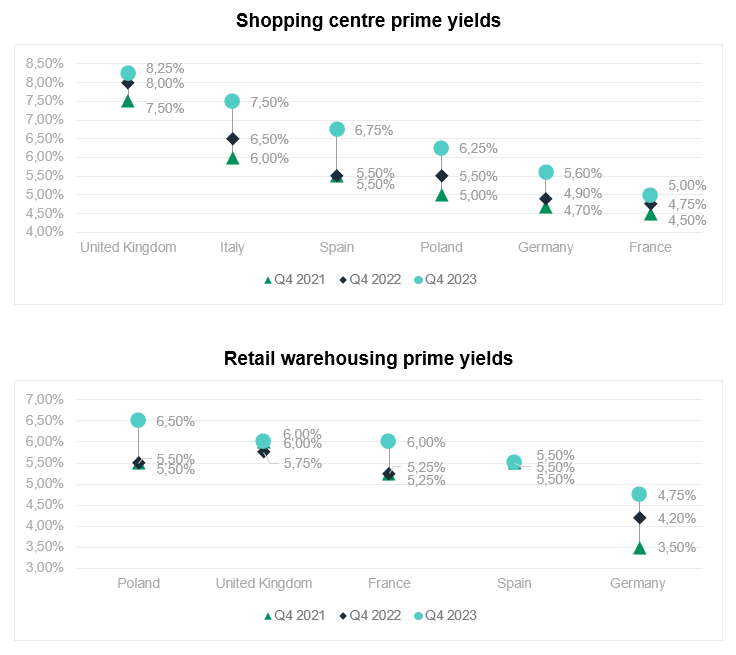

Attractive risk premium for retail warehousing and shopping centres

The rapid rise in risk-free rates in 2022 and 2023 has driven up prime yields, leading to repricing across all asset categories.

Retail prime yields started to expand in the second half of 2022 and continued to do so throughout 2023. This yield expansion remains less pronounced than for other asset categories (office or logistics), as they had already adjusted at the time of the health crisis in 2020.

“Prime yields for retail warehousing and shopping centres remain very appealing throughout Europe and continue to attract investor interest. They are the segments that offer the best risk premiums of all real estate asset categories”, remarked Patrick Delcol.

*(France, Germany, United Kingdom, Italy, Spain and Poland)

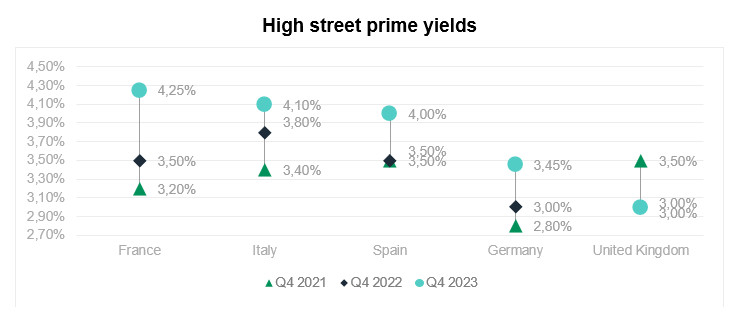

High street prime yields remain the lowest despite having widened in most countries. This situation mainly reflects buoyant transactions in the luxury sector, which has weathered the crisis well. However, this is a niche market that is far from reflecting the high-street segment as a whole, notably the struggling mass-market players.

With interest rates having peaked in late 2023 and central banks poised to lower them this year, investors should enjoy more favourable financing conditions, which should boost investment volumes in the second half of 2024 , mainly by value-add and opportunistic players in need of leverage.

Occupiers markets prove resilient, driven by luxury, innovative concepts and tourism

Luxury brands still in the spotlight

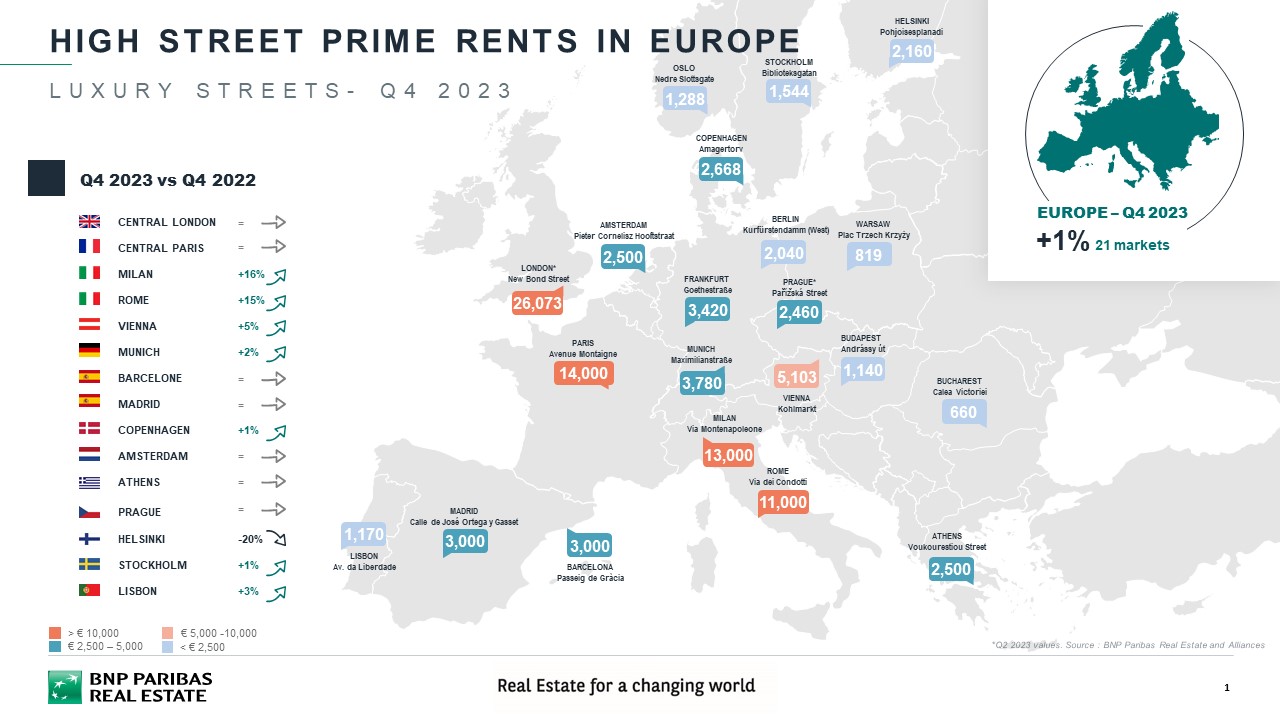

In the occupier market, luxury brands are willing to pay a high price to access ultra-prime locations, as evidenced by the record rent signed by Yves Saint-Laurent on Bond Street in London. Store openings on European prime throughfares proliferated in 2023, such as Dior on Avenida de la Liberdade in Lisbon and Schiaparelli in the prestigious Harrods in London.

The reduced availability of prime locations drove up rents on luxury shopping streets in city centres. Rental growth is particularly noticeable in Milan (€ 13,000/sqm/year, +16% in Q4 2023 vs. Q4 2022 on Via Montenapoleone) and in Rome (€ 11,000/sqm/year, +15% on the Via dei Condotti). Rental growth also occurred in Vienna (€ 5,103/sqm/year, +5% on Kohlmarkt) and Lisbon (€ 1,170/sqm/year, +3% on Avenida da Liberdade). In Paris, prime rents are stabilising, although vacancy continues to decline.

Ambitious omnichannel strategies and innovation have become paramount for mass-market brands

The cost of living crisis has exposed weaknesses in business strategies: 2023 was marked by receiverships, liquidations and restructuring of historic brands. However, for many of these names, the problems have been caused by flawed business strategies. Some players concentrated all their investment in e-commerce expansion rather than developing an effective omnichannel strategy. Conversely, brands that underinvested in digital are now struggling.

E-commerce pure-players ran into difficulties in 2023, with declining online sales and more product returns. Pure online retailers are facing competition from brick-and-mortar operators, who have been stepping up their efforts to build an integrated multi-channel model, particularly since the end of the pandemic.

The latter capitalise on click & collect capabilities, enhanced "ship from store" strategies (flexible logistics: being able to deliver orders placed online from any warehouse, distribution centre or physical store, where the product is closest to the customer), or in-store return services for products purchased on the internet with immediate refunds.

Furthermore, mass-market brands are opening innovative, state-of-the-art stores, which stand out for their superior customer experience.

In London, Fast Retailing has opened a Uniqlo-Theory store, which includes two studios where shoppers can recycle, repair or remake their Uniqlo items. They can also create their own designs. The store is home to Uniqlo UK’s first in-store café, which offers customers “Japanese-inspired refreshments”. It also has an outside terrace for relaxation.

Meanwhile, as well as selling its sportswear, Circle Sportswear’s Parisian pop-up store will host discussions between athletes and running enthusiasts. Races starting from the shop will be organised and there will also be a catering area.

In its new Parisian “General store”, which has been designed like a hardware store, the sneakers brand Veja is offering its customers a sales area as well as a shoe repair shop and tailoring service to extend the life of shoes and clothing.

Promising prospects

The outlook for European consumer spending is encouraging. The slowdown of inflation will lift real wages and consumer confidence, thereby boosting domestic consumption across Europe.

Moreover, global tourism is returning to pre-pandemic levels. International tourist arrivals in Europe rose by 17% over 2023 vs 2022. The Southern Mediterranean region is leading the recovery (+1% vs 2019), according to the World Tourism Organisation. The return of tourists is adding to footfall on Europe's main shopping streets.

“These two factors suggest that a rebound in retail sales should be forthcoming in 2024 in almost all European countries, which should support the retail industry”, concludes Patrick Delcol.

- Amira TAHIROVIC